(Stephen’s favorite board game is Hero Quest)

(Stephen’s favorite board game is Hero Quest)

In my previous post I talked about how living off the grid can help you escape the rat race. We also talked about the chains that tie us down. Some of the biggest chains are car loans, credit cards, and home mortgages. This is where the subject of debt comes in.

First we should define debt: Debt is owing someone something. This is usually in the form of money, but it can be in the form of your time or in the case of some fairy tales it can be your first born child.

Based on that definition, a work contract can put you into someone else’s debt the same way a traditional loan can. When you take on debt, demands to repay the debt control your decisions. You become an indentured servant, making money for someone else, or doing work for someone else. In other words, you’re making someone else rich.

I highly recommend reading Rich Dad Poor Dad, by Robert Kyosake. (This link is an affiliate link for Amazon. I do earn some commission from purchases you make via that link, so thank you. 🙂 )

He has a great view on debt, the rat race and controlling your money flow. Understanding the principles presented in his book will help you get control of your money and help you break the chains holding you in the hamster wheel.

The Power of Interest

Loans, mortgages, and credit cards are money making devices that banks use to get rich. These money lending tools are designed to keep you in debt and keep you earning money for the banks in the form of interest. If you can find a way not to use them, then you can keep that money for yourself. For example; by the end of a 30 year mortgage for $100,000 at 5.5% interest you will have paid the bank $104,404 in interest! More than you borrowed! If you had paid yourself that same mortgage payment you could have bought your home with cash in 15 years, instead of paying the bank for 30 years.

Instead of coming out of college and buying a $150,000 to $250,000 home, I suggest moving back in with the parents and paying yourself a mortgage. You could also rent a small apartment or join in with a friend on a place with the smallest monthly rent possible. The “best practice” for monthly budgeting currently suggests having a mortgage payment of 1/3rd your monthly income. I suggest you stick to that, but instead of paying the mortgage to a bank, you pay it to your savings account. If you make $30,000 a year, then in 5 years you could have $50,000 saved. This could buy you a small home, or single wide trailer somewhere. Then 5 years later you could sell your trailer and upgrade to a bigger home. The piece of mind gained from not owing a bank for your home is indescribable. Knowing that if you lost your job, you would still have a roof over your head is amazing.

This same principle applies to car payments. The “best practice” for monthly budgeting states, make sure that your car payment is 1/5th or less of your monthly income. I propose that you do not buy a new car with a loan. I suggest that you pay yourself that car payment. In just a few years you’ll be able to buy that car with cash. Again if you are making $30,000 a year at 1/5th paid to yourself, you would be saving $6,000 a year towards your new car. It would only take 3 years to buy an $18,000 car (including taxes). If you financed that same car at 10% interest you would pay $23,000 over 5 years. I don’t know about you, but I would rather keep my $5,000. (I also suggest not buying new because the devaluation on new cars is ridicules)

I know that this is not the way most people do it, but by doing it this way you will never chain yourself to a loan. You will also have more respect for your home and auto, because you had to save up for them. In addition, while you are saving, you get to take advantage of interest. You get to use the same money making techniques that the banks use. When you set up your savings accounts, make sure that they are interest bearing and if needed, set up a mutual fund. This way, as your money is building up, it is also working for you by making you more money. Instead of the other way around, where you are making money for the bank.

Is there such a thing as good debt?

In my opinion no, but some would argue. They would say that if you use a loan to purchase something that makes enough money to pay the monthly loan payment, then it is considered good debt. Things that could fit in this category are things like, vending machines, businesses, rental property, solar panels, wind generators, etc. You have to be careful though, because something could change and your monthly revenue may not be able to cover the loan payment. This is why I don’t like any debts. One of my biggest pet peeves is when someone says a home loan is good debt. Beware, this is something the banks have convinced America of, so they can make more money. They say that a home is good debt, because the home increases in value. I suppose it could be good debt, if the increase in value is enough to cover maintenance, insurance, taxes, and the loan interest. Odds are this is not the case.

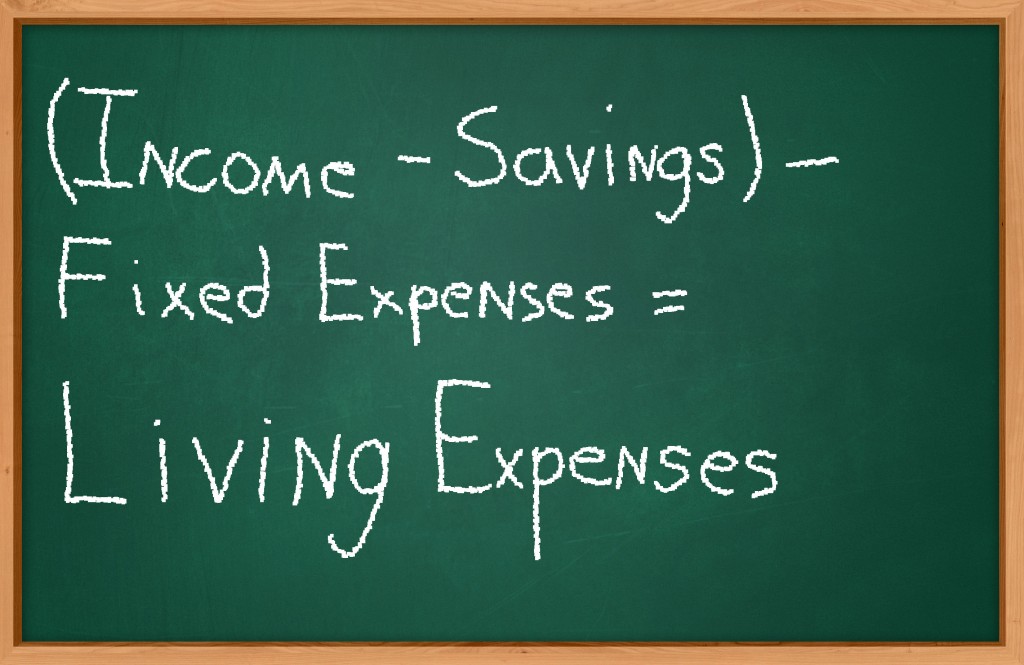

The “Get Out of Debt and Save for the Future” Formula

Getting out of debt comes down to a simple formula. If you can figure out the formula and stick its parameters, you will see results. Here is the formula and an explanation of the variables:

Income is the money coming into your household. (paycheck, rent, child support, etc.)

Savings is the money you are paying to your future self, or money that goes towards your current debt.

Fixed Expenses are the bills that you pay monthly or annually. (rent, utilities, auto insurance)

Living Expenses are your daily purchases, things that vary. Things like clothes, food, vacations, and entertainment.

It is important to notice that savings comes before expenses. You should also make it transparent, or automatic. That way you don’t think about it. If you can make your savings automatic, then all you see is the money you can spend on fixed and living expenses. Also, by using the formula above, you will make it a priority to reduce your fixed expenses, so you can have the highest possible amount of money for living expenses. The key to this formula is that savings comes before living expenses. This is important, because you take will power out of the picture. Many people make the mistake of putting savings last. Their formula looks like this:

(Income – fixed expenses) – living expenses = savings

or this:

(Income – fixed expenses) = living expenses – savings

Almost always with these formulas savings becomes zero.

In order to get out of debt, you need to create a budget and stick to it.

In effort to keep this post from getting too long I created a separate post on creating a budget. I know it can be daunting, but hopefully that guide will help you. You may also find my Excel Budget Template helpful.

Sticking to Your Budget

“Too many people buy things they don’t need, with money they don’t have trying to

impress people they don’t even like.” – Unknown

Sticking to your budget comes down to the will power not to buy. In order to gain that power you need to first know why you buy. Humans have an insatiable appetite for more, so we tend to become unsatisfied with what we have. Since enough is never enough, money cannot bring you long term happiness. Whenever you buy something you want you gain a temporary happiness. Like when you eat your favorite dessert. It makes you happy for a while, but it will shortly ware off, leaving you wanting more. If you think about how many hours of happiness something will bring you before you buy it, you’ll be able to cut out many unnecessary purchases. In addition, if you work on being grateful for what you do have, you’ll find yourself wanting less. I try to say a prayer of gratitude every night to keep me in the right mindset.

Another thing you can do to get control of this willpower, is have a goal or a mission. If you have a financial goal then you have something you can work towards. This will help making money wise decisions easier. Say you have a goal to save up $50,000 for a college fund for your kids. Every time you buy something think to yourself, “Is buying this going to get me closer to my goals.” It will help you shift your priorities and make it easier to make purchase decisions.

Finally sticking to your budget can come down to refocusing your priorities. Take a look at yourself and the priorities that cost you money. For example, is having the newest fashions a priority for you? Is playing the newest video game a priority for you? Is seeing that big game live a priority to you? Is drinking a beer every night a priority for you? Find that root cause for what ever money spending priority you have and change that priority. Make earning more money a priority. Make saving money at the grocery store a priority. Find more budget savvy priorities, and replace them with your costly ones.

Living Off the Grid Can Help You Get Out of Debt

Many of the off grid principles are cost efficient. One of the main principles is “make it yourself.” This can reduce your cost of household goods. It also has a great affect on your food cost. Not only is it cheaper to cook meals from scratch, it is also cheaper to grow your own fruits, vegetables and herbs. Composting can reduce waste and the cost of fertilizers. Depending on your skill level, hunting and fishing can cut the cost of your meat. Raising your own livestock can cut down on your meat costs as well, especially if you butcher it yourself.

Utility costs will be cheaper or non existent. Living off the grid can provide you with “free” electricity and water. If you are still connected to the grid, you can get paid for your excess electricity. You will also find yourself going out less, buying fewer frivolous things, paying less interest and enjoying life more.

Conclusion

Becoming debt free is an important step to living off the grid. In some ways it is the first step. But because it is more of a long term goal for most of us, it is something we can work on while we learn the other principles of living off the grid.

What other things can we do to stay out of debt? Or help us get out of debt faster?

I really appreciate the information here as it hit home on my debits, well I have to admit I am in 150.000 in debit and don’t even know how to get out. I am also homeless but living in a shelter right now for about 6months looking for a job part time with wanting to start my own business in which I have starts with 100 dollars or less. I agree with the budget process and using all free resources I can to help live a more economic life style that is affordable. As I am in this shelter I wanted to take advantage of this time to get on track and live off grid and to work on grid coming back home to my off grid peace of life and teach others the same, My #1 one mission is to become debit free so that I can live off grid

Hi Aisha,

Stay strong. You are not alone. Just remember that one key to getting out of debt is to make sure and set at least 10% of your earning aside for the future. Read “The Richest Man in Babylon”, it will help you understand how this concept is at the root of all wealth building and getting out of debt.